Moneyball and Disruption

Applying The Innovator’s Dilemma to the national pastime

Part of what drew me to baseball was its potential for disruption. Yes, I grew up playing the sport, and I liked the numbers, and the analytical aspect, and the strategy, and the competition. But once I realized I wasn’t going to make the major leagues as a player, I was on a path to a traditional STEM career until I read Moneyball. What captivated me and so many others about Moneyball (and other Michael Lewis books-turned-movies like The Blind Side, The Big Short, etc.), was the opportunity to find hidden value in new places with disruptive ramifications.

This isn’t just a baseball story; it’s a test case. This essay is about why Moneyball represents a genuine form of disruption—but also why that disruption does not unfold the way Clayton Christensen’s theory from The Innovator’s Dilemma would predict.

Baseball’s Markets and Incentives

The baseball industry includes a few different markets. There is the market to sell tickets, concessions, and other revenue-generating products, where teams compete against other local or broadcast/streaming sources of entertainment. There is also the market for the best players to field the best teams, which largely drives revenue generation as well. This market for players, which is the focus of this article, can be broken down into the draft, the free agent market, and other sub-markets.

How those markets are structured determines how much pressure teams feel to change. The baseball industry has monopolistic characteristics, including a Sherman Antitrust Act exemption and dominance in the roughly 27 North American markets in which it operates. There is a fixed number of teams, games, roster spots, and championships. A large portion of revenues come from broadcast deals locked in for years or decades, regardless of how compelling the on-field product is. As a result, teams are insulated from competitive threats, and the pressure to innovate is low.

Those protections produced a system that rewarded continuity over experimentation. Baseball was moderately successful and growing for most of the 20th century, with no major disruptions. There were sustaining innovations—radio, television, night games, and the internet—and some teams leveraged these better than others. But running a baseball team was largely a winning financial proposition for most owners.

The risk of upsetting the apple cart was high, and the reward for experimentation was uncertain. Thus, baseball was resistant to disruption for a century. But eventually, disruption came anyway.

The Pre-Moneyball Equilibrium

Over time, that stability hardened into orthodoxy—especially in how players were evaluated. For decades, teams evaluated and developed players using largely static frameworks and technologies: traditional scouting, the “five tools,” radar guns, and incremental improvements on those tools. Players were acquired through amateur signings, trades, the draft, and eventually free agency.

Free agency, in particular, created a seemingly efficient market for talent—but one where success depended heavily on payroll size. Large-market teams could generate more revenue, support higher payrolls, and consistently compete for the most expensive players. Small-market teams competed in the same talent markets, under the same rules, but with far fewer resources. In that environment, low-payroll teams were structurally destined to struggle.

For some teams, competing the same way was no longer an option. Unintentionally, free agency would later become the catalyst for disruption by making those constraints impossible to ignore.

Moneyball as a Different Kind of Disruption

One of those small-market teams, the Oakland Athletics, began operating differently, as documented in Moneyball. Instead of competing for the same players as everyone else, they searched for undervalued skills in players the market systematically discounted. They were not solving the same problem as large-market teams; they were solving a survival problem.

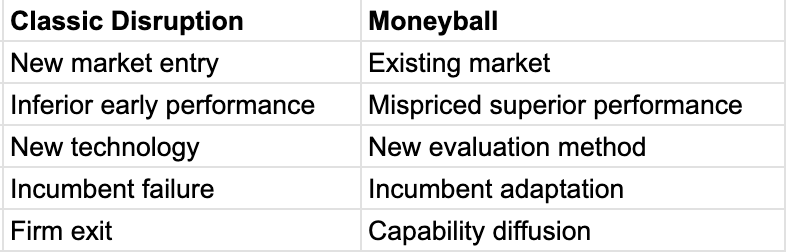

Does the Moneyball movement even qualify as a “disruptive innovation” in the Christensen sense. It doesn’t create a new market, it doesn’t begin with inferior performance, and it doesn’t drive incumbents out of business. By those standards, calling Moneyball disruptive would seem like a category error. But stopping there misses what actually changed. Christensen argues that disruption typically begins in new markets or new value chains. Baseball is different. The disruption occurred inside existing markets, using existing assets. What changed was not the supply of players, but how teams evaluated them.

This is not equivalent to the classic example of a disk drive manufacturer developing a smaller, cheaper drive for a new market and then moving upmarket. Moneyball is closer to a disk drive buyer realizing that some of the cheapest drives already perform nearly as well as the most expensive ones—and reorganizing their entire purchasing strategy around that insight. The innovation was not technological; it was epistemic. It was a breakthrough in measurement and valuation on the demand side.

Once valuation changed, replication was inevitable.

Diffusion, Adaptation, and Why Incumbents Survive

Moneyball’s publication in 2003 accelerated this shift. Ownership groups, media, and fans began demanding innovation, and teams slowly followed. Early adopters were often small-market teams with little to lose—the A’s, Indians/Guardians, and Rays—but eventually large-market teams caught on. With more resources, they were able to adopt and extend these methods, often surpassing the original innovators.

That adaptation exposes the limits of applying classic disruption theory to a protected monopoly. In classic disruption, incumbents fail because they cannot adapt in time. In baseball, incumbents adapt—and survive. Revenue sharing, competitive balance mechanisms, and monopoly protections prevent organizational failure. Poor performance may result in years of losing or leadership turnover, but rarely existential collapse. A few high draft picks, combined with an analytics-friendly front office, can reverse fortunes quickly, as seen with the Astros, Cubs, and others.

What Moneyball Really Shows

Moneyball demonstrates that disruption can occur without new entrants, without firm failure, and without technological breakthroughs—when evaluation itself is the scarce resource. In monopolistic systems like Major League Baseball, disruption does not eliminate incumbents; it reshapes how they compete.

Any industry with restricted entry and guaranteed revenue is likely to behave the same way. That makes Moneyball not an exception to Christensen’s theory, but a boundary case—one that reveals how profoundly market structure determines the consequences of innovation.